DOWNLOAD

DOWNLOAD

A CSG South First Look

In early 2025, President Trump announced via social media that he had directed the Treasury Secretary to halt penny production, citing the cost of minting the coin, which exceeded two cents per penny, as wasteful. The elimination of the penny affects more than a single transaction; it has implications for cash wage payments, tax remittance, price discrimination, gratuities, and more. Without a federal standard, policymakers, consumers, businesses, and state agencies are left to navigate questions of compliance and liability on their own.

Activity in 2025

Limited Federal Action

Congress introduced two “Common Cents” bills in April 2025. US HR 3074 and US S 1525 would formally direct the Treasury to cease minting the penny, and establish in-person cash transaction price-rounding rules. Lawmakers propose rounding total prices, after the application of sales or other taxes, to the nearest five cents. Canada adopted this method of price-rounding when the nation ceased production of its respective one-cent coins. Under this policy, entities would round cash transaction totals ending in $0.01, $0.02, $0.06, or $0.07 down to the nearest nickel, and round totals ending in $0.03, $0.04, $0.08, or $0.09 up to the nearest nickel.

Federal lawmakers took limited action on the Common Cents bills during the remainder of the year as Congress focused on other policy and fiscal issues, including the federal budget, healthcare, SNAP, and a government shutdown.

States Take the Lead

Although billions of pennies remained in circulation, localized distribution caused regional shortages in the penny supply in November. Without national guidance, confusion, inconsistency, and potential implications for consumers, business, and state revenue emerged, prompting state lawmakers across the country to try to tackle the time-sensitive issue.

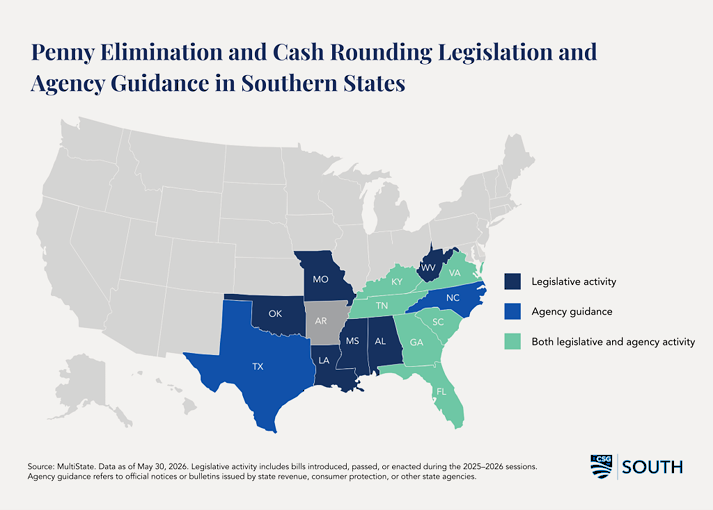

2026 Southern States Legislative Landscape

Penny elimination has been one of the most active legislative issues this session as legislators in 34 states considered 60 bills. As of this writing, 19 bills have been enacted, 3 bills that passed the legislature, and 5 bills that passed their chamber of origin. In Southern states, the governors of Alabama, Florida, Georgia, Kentucky, Oklahoma, Tennessee, and Virginia signed penny elimination legislation into law.

The majority of legislation introduced in 2026 follows the Canadian rounding method, establishing some uniformity despite the varying approaches across states. Bills introduced in Florida (FL HB 951 & FL SB 1074), Missouri (MO HB 2819) and South Carolina (SC HB 4617) align with the price-rounding method introduced in Congress (US HR 3074 & US S 1525).

By the end of January, bills from Mississippi, Tennessee, and West Virginia also proposed to round cash transactions following that same method. In Kentucky, penny elimination requirements were enacted as a provision included in the state’s revenue bill KY HB 757.

By March, several states had enacted the first penny elimination laws. Among southern states, Tennessee enacted TN HB 1744 that month. Arizona, Indiana, New Mexico, Utah, and Washington also enacted legislation in March, reflecting the rapid pace of activity nationally. Louisiana took a preliminary step, with legislators introducing LA HR 252, which urges the attorney general to study the impacts of penny cessation, including, but not limited to, uniform rounding standards, disproportionately affected communities, and credit card fees by businesses.

Nationally, the Utah Division of Consumer Protection was the first state agency to issue guidance on cash rounding. Utah’s guidance recommended the same symmetrical rounding method proposed in the federal bills. In New York, companion bills NY A 9274 / NY S 8580 propose the same rounding approach. While early state action on guidance and legislation was concentrated outside the South, southern lawmakers moved quickly in the 2026 session to address the issue.

Other Provisions Impacting Southern States

Tax Calculation and Remittance

Agency guidance on penny elimination initially focused on recommending rounding methods. Kentucky’s Department of Revenue, for example, issued early guidance on symmetrical rounding for retailers, but state revenue departments quickly turned to a more pressing question: how does rounding affect sales tax? If a retailer rounds a $0.98 purchase up to $1.00, should sales tax be calculated on the original amount or the rounded total?

Several southern states have weighed in. Florida, Georgia, North Carolina, and Tennessee each issued guidance requiring retailers to calculate sales tax on the pre-rounded transaction total, regardless of which rounding method the retailer applies. These notices leave the choice of rounding method to individual retailers while clarifying that rounding does not alter the amount of tax owed to the state. The Texas Comptroller of Public Accounts took the guidance a step further, specifying that if a retailer rounds to an amount other than the nearest nickel, the Comptroller will recalculate the sales price and the tax owed accordingly. South Carolina’s Department of Revenue similarly confirmed that the correct sales tax must be remitted regardless of the rounding method.

Form of Payments: Cash Acceptance

The retail cash acceptance trend presents an additional complication for price-rounding rules. Nine states, all outside of the South, currently have laws requiring retail businesses to accept cash, and some include provisions prohibiting businesses from charging cash-paying customers more than those paying electronically. That restriction may create potential conflicts with symmetrical rounding: any transaction rounded up to the nearest nickel would effectively cost a cash customer more than the stated price. Southern state lawmakers are engaging with the cash acceptance issue this year.

Legislation proposed in Alabama (AL HB 526) and Tennessee (TN SB 739) would have required entities with six or more employees to accept cash for in-person transactions. Tennessee’s measure and another in Virginia (VA HB 984) also included language prohibiting cash customers from being charged more than their electronic counterparts. West Virginia lawmakers introduced WV HB 4060, which would have required businesses, including retail food establishments, to accept cash. In Louisiana, Governor Landry received LA HB 308 for signature, which if signed would require public stadium facilities to accept cash for in-person transactions.

Agency and Political Subdivision Payments

State lawmakers initially focused on retail settings, but quickly recognized that cash transactions in government and agency contexts raised the same rounding questions. Lawmakers in Mississippi (MS SB 2847), Oklahoma (OK SB 1397), and Virginia (VA HB 954) considered rounding methods for various payments to government entities, including tax bills. Another bill from Mississippi (MS SB 2874) proposes rounding governmental cash transactions to the nearest dime, not nickel. Virginia’s Alcoholic Beverage Control Authority (ABC) announced implementing potential price differentials of ± $0.02 on distilled spirits and similar products sold at ABC stores beginning February 1, due to the penny shortage. The liquor authorities in other control states such as Alabama, Mississippi, North Carolina, and West Virginia may need to adopt similar price adjustment policies for cash transactions at state-run retail outlets.

What Happens Next

Emergency clauses have already put many recently enacted state legislation into effect. Lawmakers in these states are likely to propose additional measures to regulate price rounding in broader contexts, such as within state agencies, and future legislation may also address rounding for cash wage payments, including paycheck cashing. As states continue to evaluate fiscal conditions and budget priorities, some states may look to extend rounding provisions to other types of tax payments as a way to protect revenue. Whether Congress ultimately establishes a uniform national standard or leaves states to set their own course remains to be seen.